Managing a consumer lending operation today can feel like juggling fire while walking a compliance tightrope. On one hand, there’s constant pressure to maximize profitability; on the other, the regulatory web keeps getting more complex. Add to that the need to deliver a seamless digital experience, and it’s no wonder many lenders feel stretched thin. So how do you maintain profitability while steering through ever-increasing regulations and preserving a stellar consumer lending customer service experience?

The answer isn’t a choice between the two—it’s about balancing both. And the smartest lenders are doing that by redesigning their operational models, partnering with the right specialists, and investing in more innovative consumer lending solutions.

Finding the Right Balance: Costs and Customer Experience

The consumer lending landscape has evolved dramatically in the digital era. With growing risks and regulatory scrutiny, adhering to compliance standards—from fair lending to data privacy—has become a make-or-break factor.

Meanwhile, digital-native fintech companies are challenging traditional banks at every step. As customers increasingly manage their finances online, traditional lenders must modernize their infrastructure and customer experience or risk losing relevance.

According to KPMG’s Banking Cost Transformation Survey, financial institutions are targeting 10% cost efficiencies within 12 months and up to 30% over three years. But cost-cutting cannot come at the expense of compliance. The winning approach is to find synergy among efficiency, trust, and experience—powered by technology and banking support services.

Step 1: Map Your True Cost of Compliance in Consumer Lending Customer Service

Most lenders underestimate the real cost of compliance. Legal fees, audits, and regulatory reporting are visible, but hidden inefficiencies eat into profitability. Manual document reviews, departmental silos, and repetitive verification processes slow down loan approvals and frustrate customers.

Start with a comprehensive audit of your compliance costs across the lending lifecycle:

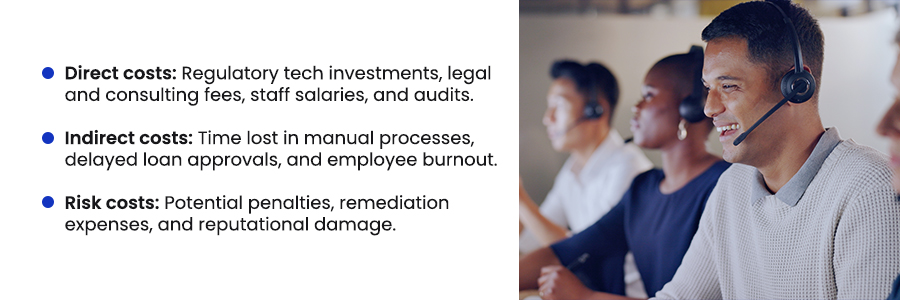

- Direct costs: Regulatory tech investments, legal and consulting fees, staff salaries, and audits.

- Indirect costs: Time lost in manual processes, delayed loan approvals, and employee burnout.

- Risk costs: Potential penalties, remediation expenses, and reputational damage.

Once you identify bottlenecks, you can redesign workflows that serve both compliance and customer experience goals.

Step 2: Identify Where Compliance and CX Collide in Consumer Lending Customer Service

Many compliance pain points are also pain points in customer experience. For instance, customers often upload the same document multiple times — a compliance inefficiency and a CX nightmare rolled into one.

To balance both priorities, lenders can:

- Audit and streamline documentation workflows.

- Simplify customer validation and eligibility checks.

- Reduce manual underwriting loops with guided automation.

- Use clear communication templates to explain compliance requirements.

- Ensure consistent regulatory communication across all channels.

The goal is to embed compliance seamlessly into the customer journey—transforming it from a roadblock into a trust-building element of customer experience in consumer lending.

Step 3: Use Technology to Turn Compliance into a Competitive Advantage

Technology is the catalyst that can turn compliance from a cost center into a differentiator. With the right consumer lending solutions, lenders can achieve operational speed, transparency, and compliance accuracy.

Automated compliance checks

- Real-time data validation against regulations.

- Automated document verification across channels.

- Instant eligibility and KYC screening to reduce manual errors.

Integrated compliance systems

- Centralized data and document management portals.

- Audit-ready workflows with zero duplication.

- Unified compliance dashboards for regulators and internal teams.

AI-powered underwriting

- Machine learning models that align lending decisions with regulatory frameworks.

- Predictive insights that reduce risk and bias.

Technology doesn’t replace compliance teams—it empowers them to work smarter, faster, and more transparently.

Step 4: Build a Compliance-Embedded Culture in Consumer Lending Customer Service

Even the best tech can’t fix a culture that treats compliance as an afterthought. To build a sustainable foundation, compliance needs to be part of every role and department.

According to Deloitte, over 80% of banking executives cite cultural resistance as a significant barrier to cost reduction and compliance transformation. The solution? Empower every team member to own a piece of compliance.

Practical ways to embed compliance into your culture:

- Train customer service reps to recognize red flags early.

- Provide clear, accessible compliance guidelines to underwriters.

- Equip collections teams with compliant communication templates.

- Make compliance performance part of departmental KPIs.

When compliance becomes a shared value, it stops being a bottleneck and becomes a growth enabler.

Step 5: Evaluate Strategic Outsourcing for Banking Support Services

Building a world-class consumer lending customer service operation in-house while managing compliance is expensive and resource-intensive. That’s why more BFSI leaders are turning to specialized partners for banking support services.

According to industry reports, over 80% of financial institutions now rely on strategic outsourcing to boost compliance efficiency and scalability. The benefits are clear:

Compliance expertise at scale

- Dedicated teams trained in CFPB regulations and fair lending practices.

- Standardized workflows to ensure consistency.

- Ongoing updates to reflect the latest regulatory changes.

Technology infrastructure

- Proven platforms with embedded compliance tracking.

- Automated documentation with audit trails.

- Real-time error detection and reporting.

A trusted partner can help lenders achieve higher profitability and compliance harmony while maintaining exceptional customer experience in consumer lending.

The Path Forward: Compliance as a Growth Enabler

The most successful lenders no longer view compliance as a constraint but as a catalyst for innovation. When you can originate loans faster and meet every regulation flawlessly, profitability follows naturally.

With the Fusion CX automation, and strategic partnerships, lenders can scale efficiently while strengthening trust. The question isn’t whether compliance and profitability can coexist—it’s how quickly you can align them.

Because in the end, the leaders in consumer lending will be those who blend compliance precision with customer empathy and operational excellence.

Partner with Fusion CX today to build compliant, profitable, and customer-centric consumer lending operations. Our expert banking support services and technology-driven consumer lending solutions empower your brand to stay ahead of risk, regulation, and competition.

Manish Jain

Manish Jain is the Chief Marketing Officer at Fusion CX, leading brand, growth, and go-to-market strategy across industries. He works closely with sales, delivery, and leadership teams to position customer experience as a driver of measurable business impact—bringing clarity, creativity, and momentum to how CX stories are told.